Higher FICO scores equal lower interest rates

A good credit score is crucial for both your personal finances and your ability to become a homeowner.

Yet many home buyers begin their journey without fully understanding their credit score and how it impacts their mortgage eligibility.

Raising your credit score fast can be done, and these tips may help you afford your dream home sooner than you thought possible.

10 Tips to increase your mortgage FICO score

It’s true that having a higher credit score will lead to better loan offers and lower interest rates on your mortgage loan.

While it can take months to overcome some derogatory credit events like missed payments, and years to build excellent credit, you can raise your score quickly with these 10 credit insights.

- Get your free credit score

- Dispute any errors

- Make on-time payments

- Pay down debt

- Become an authorized user

- Consider a rapid rescore

- Never carry a credit card balance

- Improve your debt-to-income ratio

- Avoid closing open bank and credit accounts

- Don’t open new credit cards or loans

Being proactive early on in your home-buying process may result in getting both the mortgage loan and home you want at a price you can afford.

1. Pull your free credit reports

Every credit repair plan should begin with reviewing your credit files from each of the three credit reporting agencies: TransUnion, Equifax, and Experian.

Under the Fair Credit Reporting Act (FCRA), you can obtain a free copy of your credit reports each year from AnnualCreditReport.com

When reviewing your credit files, look for:

- Negative information that could be lowering your credit score: Too many hard inquiries, low available credit, late payments, collection accounts, and high credit utilization ratio are examples we’ll describe below

- Credit reporting errors: Unexplained or unauthorized credit card debt, lines of credit, or new accounts — such as new credit cards, auto loans, or bank accounts — could be instances of fraud or mistaken attribution by credit bureaus or credit card issuers

2. Dispute negative information

According to the Federal Trade Commission (FTC), credit errors are alarmingly common.

Under the FCRA, you have the right to challenge any errors with the relevant credit agencies, and they must investigate your dispute within 30 days.

Correcting and reporting errors that are lowering your score should be at the top of your speedy credit improvement to-do list.

“It’s important to immediately dispute all claims made against you that are false on your credit report,” says Steven Millstein, a certified credit counselor with Credit Zeal.

You could also pay credit repair companies to file disputes for you. However, the Consumer Financial Protection Bureau (CFPB) publishes free dispute letter templates to help you manage this process on your own.

3. Make all payments by their due dates

Making on-time monthly payments for your household utility bills, cell phone services, and installment loans — like personal loans and student loans — is an important component of building excellent credit.

“Try setting up automatic payments through your lender or financial institution,” says Daryn Gardner with Jax Federal Credit Union. “And always pay on time the minimum payment stated on your bill.”

Missed payments and late payments are among the biggest contributors to bad credit scores.

4. Pay down credit card debt

FICO and VantageScore credit scoring models both pay close attention to your credit utilization rate.

Credit utilization is the percentage of credit you’re using compared to your total available credit limits across all of your revolving credit lines.

If you have a $10,000 balance on a credit card with a $20,000 credit limit, then your credit utilization ratio is 50%.

“The most effective way to improve your credit score is to pay down your revolving debt,” suggests Gardner. “Apply your tax refund to pay down your debt.”

You may be able to improve your score simply by replacing credit card balances (revolving credit debt) with a personal loan (installment loan debt).

Additionally, if your credit card company will grant you a credit limit increase, that can also improve your credit utilization rate.

5. Become an authorized user

If your problem is that you have a limited credit history, becoming an authorized user may help you build credit.

You can get a boost by having family members or friends who have excellent credit, and even good credit scores, add you to their accounts as an authorized user.

You don’t actually use these accounts. But your family’s good payment history will appear on your credit report. On-time payments will help you raise your credit rating.

Be aware that becoming an authorized user can also negatively impact your credit ranking if your family member’s account ever has high balances or late payments.

6. Ask your mortgage lender about a rapid rescore

If you need errors corrected quickly, ask your lender about rapid rescore services.

Disputing errors on your credit report can take months. Similarly, it can also take a long time for credit card issuers to report changes once you pay down debt.

Rapid rescoring can issue you a new credit score in a matter of days, instead of months, once you’ve done the hard work of credit repair.

Keep in mind that only your mortgage lender can get this for you because rapid rescore services don’t deal directly with home buyers.

“Rapid rescoring can be ideal because your lender can run a simulation to tell you the best course of action to bump up your credit scores,” says Jon Meyer, The Mortgage Reports loan expert and licensed MLO.

7. Don’t max out your credit cards

Using credit cards responsibly can help build your credit. But spending up to your credit limit will hurt your score.

“Only charge as much as you can reasonably pay off within a given month,” Millstein notes.

To get the best scores, try to keep all your credit cards below 30% of their available limit.

8. Improve your debt-to-income ratio

Debt-to-income ratio (DTI) is an important factor in your mortgage qualification. The lower your DTI, the better your chances of getting approved for a home loan — and the lower your interest rate.

Paying down your debt not only improves your debt-to-income ratio (DTI) but also boosts your credit score. Calculate your DTI by adding up your expenses and dividing it by your gross monthly income.

“Say your monthly income is $1,500. Say your total monthly expenses are $800. Divide the former by the latter to get 53%,” Millstein says.

He adds that “lenders prefer your DTI to be 43% or lower.”

9. Avoid closing accounts before applying for a loan

Remember that the average age of your credit is an important factor in your credit score. Credit bureaus like to see a long history of well-managed accounts.

“The longer the info remains on your report, the better it is for your credit score,” says Millstein.

So even if you have a credit card paid down to zero, you don’t want to close that account prior to applying for a mortgage loan.

“With credit, you use infrequently, try making a small purchase from time to time. This prevents your account from becoming inactive,” Millstein suggests.

10. Avoid applying for new credit cards and loans

If you’re thinking about buying a home in the foreseeable future, apply for new types of credit carefully.

“Don’t try applying for more than three new credit accounts in a single month,” cautions Millstein. “Your credit score is greatly affected by the number of credit inquiries made to your credit report.”

Furthermore, choose merchants that are more likely to approve you. “Aim for a secured credit card at your local bank, department store, or fuel merchant,” adds Millstein.

In the months leading up to your mortgage application, avoid opening any new accounts at all. This can increase your DTI and lower your score in one fell swoop.

“Also, avoid making any large purchases [prior to getting a mortgage],” says Meyer. Wait to finance furniture or buy a new car until after closing day.

How quickly can you improve your FICO score?

If all you need is error correction, you may see your FICO increase in a matter of days. However, there is no guarantee that correcting errors will make your score go up.

Paying down significant amounts of debt — say, dropping your credit utilization rate from 80% to 20% — can also bump your score up rapidly.

But if your credit report is littered with late payments collections or other serious problems, Gardner says it can take “up to 12 months to raise your score.” You must first demonstrate a consistent payment history.

Understanding credit scores

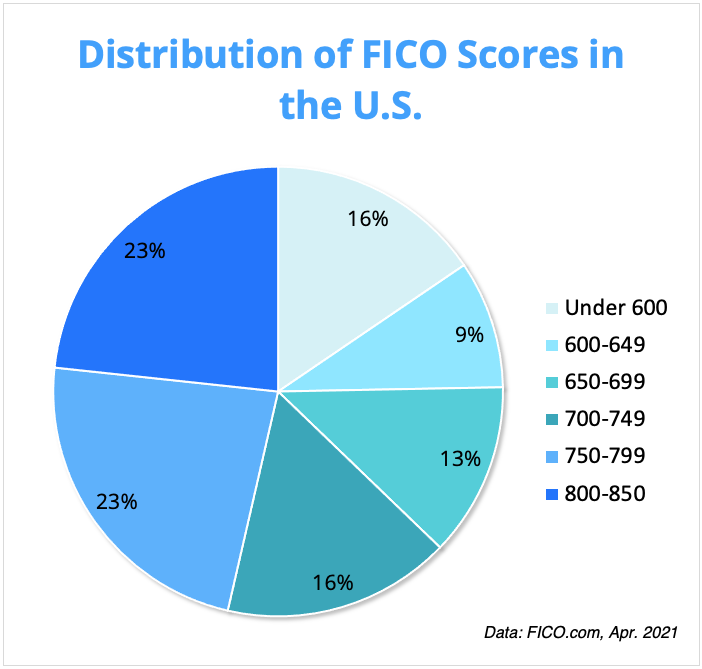

Your credit score, also called a FICO score, is a three-digit value ranging from 300 to 850. This number indicates how likely you are to repay your debt. This score is based on info in your credit report that comes from the three major credit bureaus: Transunion, Equifax, and Experian.

“Any score above 670 is considered very good. Anything below 600 is considered weak,” says Lou Haverty, a chartered financial analyst (CFA).

A higher score gets you to access to better home loans. That’s very important when buying a home, says Gardner.

“For example, a high credit score borrower may be offered a 30-year fixed-rate loan at 4%,” he says. “An average credit score borrower may be offered the same loan at 5%. On a $200,000 loan, the average-score borrower would pay $40,000 more in interest over the life of the loan.”

What determines your credit score?

Five factors make up your FICO score calculation:

- Payment history: 35% of your score

- Credit utilization ratio: 30% of your score

- The average age of credit: 15% (a longer credit history will raise your score)

- Credit mix: 10% (a mix of installment accounts like car loans are better than revolving credit accounts like credit cards)

- New credit: 10% (opening too many new accounts and having too many credit inquiries over a short period can lower your score)

An improvement in any of these categories can help boost your credit score. But to see the biggest impact, make sure you pay all your credit accounts on time and keep your credit balances below 30% of their total limit.

Check your home buying eligibility

The bottom line, improving your credit score quickly is possible.

However, the amount of work you’ll need to do and the speed at which your credit rating will rise both depend on your current personal finances.

Connect with Mortgage Mario today to discuss your financial situation and whether or not a rapid rescore will work for you.